The most basic rule of accounting is that one person’s spending equals another person’s income. If I lend ten pounds to you, then I am ten pounds poorer while you are ten pounds richer; for every credit (+ £10) there is a debit (-£10) and if you put these two figures together, they always sum to zero ( +£10 -£10 = £0).

This simple operating principle applies not just at the personal level but to the economy as a whole: deficits and surpluses must always cancel out across the financial system.

In any economy, three sectors interact financially:

- The Government sector (public)

- The Private sector (households + businesses)

- The Foreign sector (rest of the world)

There’s an iron-clad accounting identity: these three sectors’ financial balances must sum to zero. One sector’s deficit is another’s surplus — by definition, not by policy.

This principle is central to the ‘Sectoral balances framework’ for understanding the wider economy.

What the Sectoral Balance Framework does

The Sectoral Balance Framework is part of the UK Office of National Statistics data and divides the economy into three broad blocks: the public sector, the private sector and the foreign sector.

- The private sector (domestic households and businesses, including financial institutions).

- The government sector (the issuer of the currency which adds and removes £s as it invests into the economy and taxes back. It also includes regional and local government).

- The foreign sector or ‘Rest of the World’ (representing trade and financial transactions with the rest of the world).

Its principal insight is that one sector’s surplus must necessarily be matched by a deficit in another, as all financial transactions balance across the economy to zero. This means that:

- If the government sector has a budget deficit, the non-government sectors (private domestic sector and foreign sector) together must have a surplus.

- And if the government sector is borrowing, the other sectors taken together must be lending.

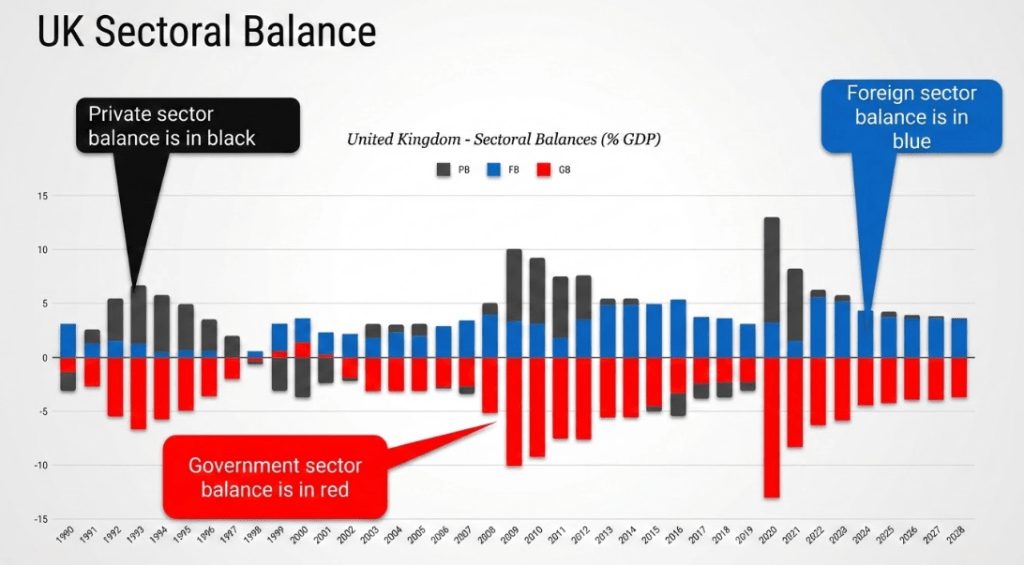

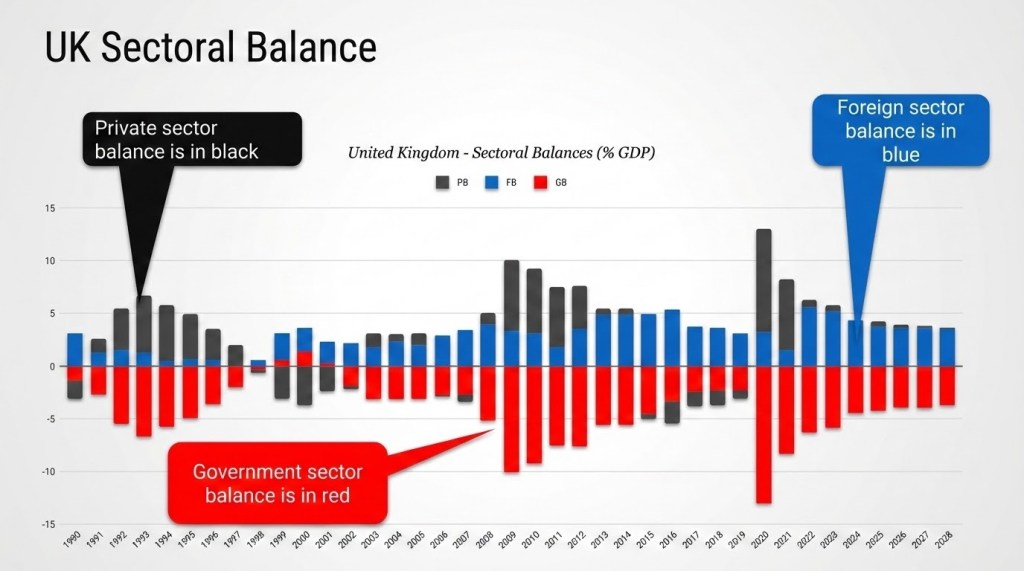

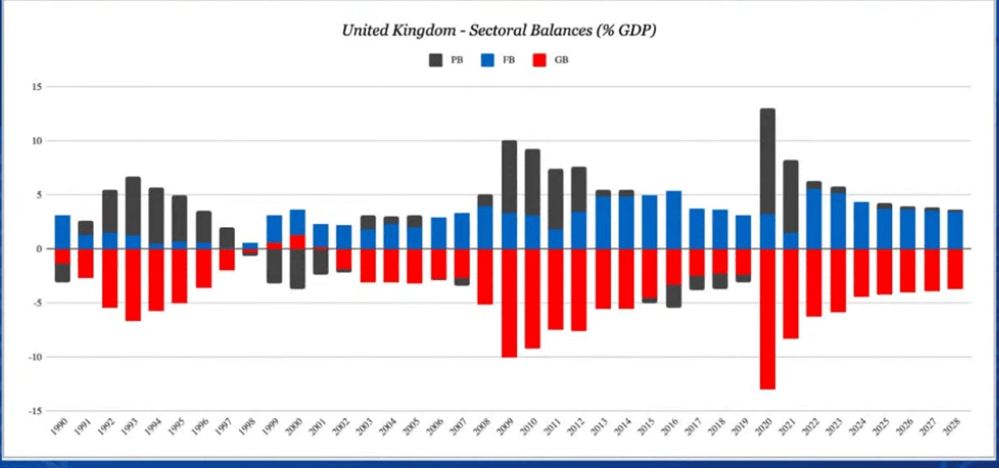

By examining the financial flows between these sectors, sectoral balances offer a comprehensive view of how economic activity is distributed and sustained. The bar chart below shows the sectoral balance for the UK.

Why does this matter?

If the government sector is in deficit, then by the rules of accounting, the private sector (that’s you, me, all households, all private businesses) must be in surplus.

It is impossible for the government sector, the private sector and the foreign sector to run surpluses at the same time.

This challenges the assumption that government deficits are always ‘bad’ as well as the fallacious claim that government budgets must always balance. Indeed, if the government sector does not go into deficit on a regular basis (i.e. spends more money than it taxes back), then the private sector cannot acquire net financial assets.

Look again at the Public Sector deficit for the UK below: this is the partial picture we are constantly given by our media, our politicians and policy pundits when they agonise about public deficits and the need for ‘responsible government’ to balance the budget.

Now look again at the sectoral balance which gives the full picture

You will see that the Government Deficit is mirrored by Private Savings – people (that’s us) and private businesses – along with savings by the Foreign Sector (rest of the world). Every liability is necessarily matched by an asset held elsewhere within the financial system. The crucial question that the media consistently fails to address is: who possesses this corresponding asset?

To stress again, the three sectors always have to balance. As Professor Randall Wray points out, the Sectoral Balance Framework demonstrates “the important accounting principle that the sum of deficits run by one or more sectors has to equal the surpluses run by the other sector(s)”. Surpluses and deficits always add up to zero.

Deficits fund savings

Government deficits fund savings. If the government is in deficit, then savings in the Private Sector and the Foreign Sector go up. Each annual deficit adds to the total ‘National Debt’.

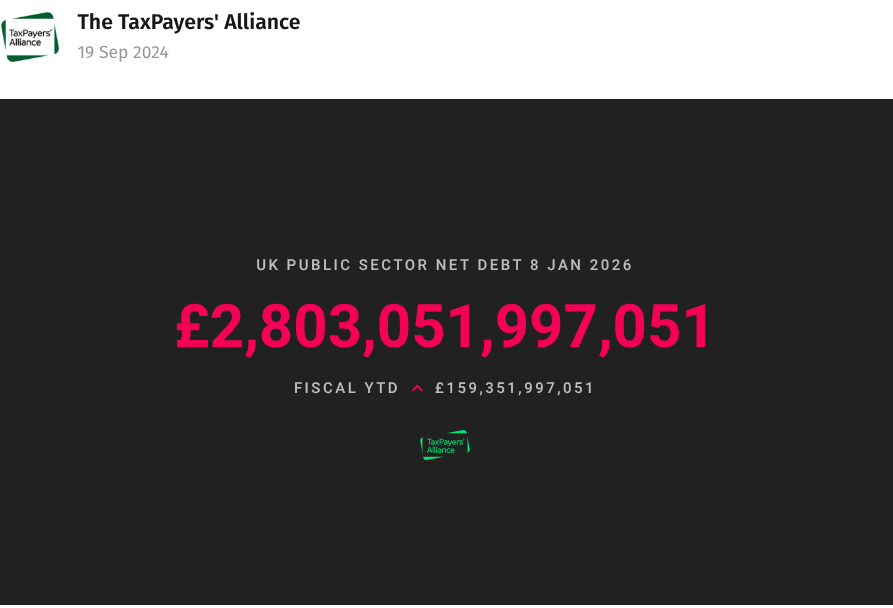

So when the right wing Taxpayers Alliance sound the alarm about growing national debt to the tune of £2.8 trillion and rising, they are also showing the private sector’s increasing financial wealth. However, under our present regressive tax system the size of the financial cake is grossly skewed towards the rich taking the largest slice of the cake. Wealth in the form of profits and dividends is also funnelled out of the UK (the Foreign Sector is coloured blue).

Nevertheless, the key points to hold onto are:

- Government deficits are private sector savings and part of the equation defining GDP.

- Government deficits are the norm, not the exception. They are neither evidence of irresponsibility nor reasons for alarm.

The myth of the “Household” Analogy (Political Rhetoric)

The Sectoral Balances Framework completely undermines politicians who often compare a country’s budget to a household budget. Government spending is nothing like that. Governments necessarily have to go into deficit if money is to be acquired by the private sector. By contrast, governments who seek to balance budgets by cutting spending withdraw money from the economy and thereby diminish Private Sector Savings.

Unlike a household, the UK government is the monopoly issuer of its own currency (Sterling). It doesn’t need to “find” money before it spends; it creates the money through spending. However, the household analogy remains a powerful and intuitive tool because politicians count on public ignorance of government finances and how they work.

Government spending and inflation

This is not to say that government deficits don’t matter, they do. When more money chases after the same number of goods or assets, the result is inflation, which can damage the economy. Reckless government spending is clearly irresponsible, but so is willful underspending which results in welfare cuts to the most vulnerable as well as budget cuts to vital public services and local government.

Government spending and debt

The fact that the UK government is the monopoly issuer of its own currency offers far more policy space for spending than politicians and media pundits claim. In particular mainstream economists vigorously push back at arguments put forward by Modern Monetary Theory that governments can and should spend in ways that benefit society as a whole, rather than the narrow fixation on maximising the role of the market. While mainstream economics does acknowledge the accounting identity that the Sectoral Balances Framework provides — it cannot deny it, because it is arithmetic, it interprets it very differently from the way the sectoral balances framework presents it.

The mainstream economics view broadly accepts that:

- Government deficits can be necessary and useful during recessions

- Fiscal stimulus can boost demand when the private sector is paralysed

- Austerity during a downturn can be self-defeating

But on the whole, it is reluctant to go much further than that. It would say: yes, deficits arithmetically correspond to private sector surpluses, but that does not mean deficits are always desirable — because the size of the economy, the inflation rate, the interest rate, and market confidence all matter too, and a deficit that is too large or persists too long can cause serious harm even if the accounting identity always holds.

In particular it will point to the present size of the national debt UK government deficits—where spending exceeds tax revenue—are considered concerning because they raise national debt, forcing higher interest payments (forecast at £111 billion) that drain resources from public services. But this overlooks two key points:

- a government with its own sovereign currency (the UK has the Pound, the US has the dollar) need not borrow from financial markets at all. It could simply instruct the Bank of England to credit its account with any amount of money in needed.That it borrows at all is because of the government’s self-imposted fiscal rules which state that any spending beyond tax revenue must be financed by borrowing.

- The interest on government debt is not determined by financial markets (so-called bond vigilantes) but the Bank of England. The Bank of England sets the policy rate on debt interest primarily to control inflation. The higher the rate set by the Bank of England, the greater the interest rate on government debt that the UK government has to pay. However, the Bank of England policy rate is a blunt instrument that do not take account of supply-side shocks such as the wars in Ukraine and in Iran.

To be clear, both the Bank of England interest rate and the government’s fiscal rules are policy choices, not choices imposed from outside.

Conclusion

The Sectoral Balances Framework clearly demonstrates the positive value of government deficits. This is the norm, not the exception and the private sector cannot acquire net financial savings without government deficits. As such it demonstrates that the government has much more policy space for spending into the economy than mainstream economics admits. The threat of Inflation matters, but this is an often over-worked objection that ignores the damage done by underinvestment in vital public services and infrastructure.

Leave a comment